Australia Family Trust Tax Reform: Big Changes Ahead for Trust Owners in 2025

Estimated reading time: 9 minutes

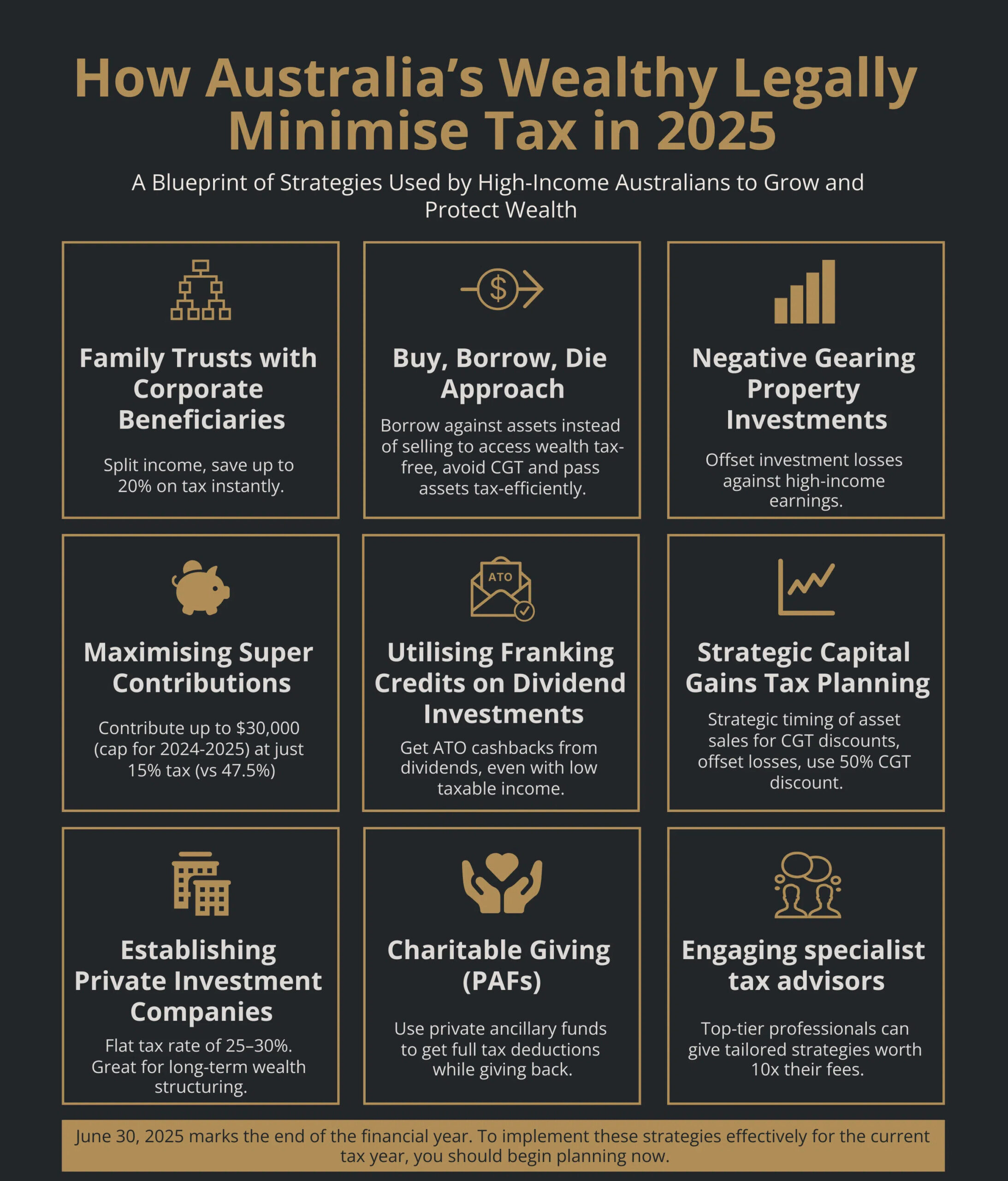

Key Takeaways

- Australia’s 2025 family trust tax reform introduces a 30% minimum tax rate on distributions to non-participating adult beneficiaries, changing the way family wealth is managed.

- Enhancements to ATO oversight mean stricter compliance for trust distribution resolutions—and harsher penalties for sloppy paperwork.

- Tax advantages of distributing trust income to low-income adult children will be minimized by the new rules.

- Capital gains tax strategies via trusts are under scrutiny and may face higher tax bills after reform.

- With the changing landscape, using a tax calculator is more important than ever for planning.

- Proper documentation and meeting the June 30 trust distribution deadline are now critical to avoid top tax rates.

- The reforms may impact small businesses, property investors, and those with business structures involving trusts.

Table of contents

- Australia Family Trust Tax Reform Takes Center Stage

- The 30% Minimum Tax Rate: A Game-Changer for Trust Distributions

- ATO Tightening the Screws on Trust Compliance

- Trust Distribution Resolutions: The June 30 Deadline Becomes Critical

- Labor’s Broader Trust Reform Agenda

- The Personal Tax Rate Gap: A Key Target for Reform

- Compliance Challenges: Navigating the New Trust Landscape

- Capital Gains in the Crosshairs

- The Practical Impact on Australian Families and Businesses

- Key Dates and Implementation Timeline

- Expert Recommendations: Adapting to the New Reality

- Frequently Asked Questions

Australia Family Trust Tax Reform Takes Center Stage

Australia’s family trust landscape faces its most significant overhaul in decades, as lawmakers target reforms for 2025. The changes aim to close loopholes, boost government revenue, and make Australia’s tax system fairer in the eyes of regulators and the public.

The Australian Taxation Office (ATO) has put trusts under a microscope, intensifying inquiries as lawmakers discuss how best to reshape tax policy for modern wealth management.

For families using trusts to administer wealth, invest in property, or operate small businesses, the implications could be dramatic—changing who gets taxed, how much, and the flexibility of traditional trust strategies.

The 30% Minimum Tax Rate: A Game-Changer for Trust Distributions

Front and center is the newly proposed 30% minimum tax rate for trust distributions to non-participating adult beneficiaries.

This provision aims to shut down strategies where high-earning parents stream income to adult children or relatives in lower tax brackets—a technique that could save tens of thousands in tax under previous rules.

Now, any such distributions will be taxed at no less than 30%—eliminating much of this benefit. Regardless of a beneficiary’s personal marginal tax rate, trusts must withhold and pay at this new minimum.

ATO Tightening the Screws on Trust Compliance

The ATO is not waiting for full legislation. Crackdowns on trusts used mainly for tax reduction are escalating.

If distributions aren’t made as declared, or funds distributed on paper stay in the trust, the ATO may nullify the resolution—taxing all disputed income at Australia’s highest marginal tax rate: 47%.

This means even minor compliance missteps could trigger a severe tax hit.

Trust Distribution Resolutions: The June 30 Deadline Becomes Critical

Every discretionary trust in Australia must now have a formal distribution resolution finalized by June 30 each year.

Missing this deadline or lacking proper documentation results in all trust income being taxed at the highest marginal rate, not the beneficiary’s rate.

Even trusts with little or no income must comply. Staying on top of this resolution has become a non-negotiable for trust administration and future-proofing against end-of-financial-year ATO deadlines.

Labor’s Broader Trust Reform Agenda

Reportedly, the Labor government has an even wider net in mind.

Future changes may home in on any distribution seen as tax avoidance—making ongoing political developments vital for trust owners.

The Personal Tax Rate Gap: A Key Target for Reform

Mismatches between personal top rates and trust rates drive much of the tax-minimization appeal.

Without aligning rates, attempts at reform may fall short. Wider personal tax return changes may be coming, signaling broader shifts in Australia’s entire tax system.

Compliance Challenges: Navigating the New Trust Landscape

Trustees, accountants, and beneficiaries now operate in an environment with little margin for error. Every trust—no matter how income-poor—must meet new standards for annual resolutions.

ATO guidance for declaring trust distributions on tax returns puts additional onus on beneficiaries. For distributions already subject to the family trust distribution tax, reporting requirements may differ.

Ongoing compliance can be daunting, but preventing mistakes is crucial—not just for high-income earners, but for anyone using a trust to manage assets.

Capital Gains in the Crosshairs

Capital gains tax (CGT) arrangements, particularly regarding trust-held investment properties and shares, are now under the microscope.

The reforms aim to block “tax arbitrage” where trusts have historically facilitated sophisticated tax planning using differential rates for CGT, income, and entities.

This could dramatically affect the after-tax returns from property sales and other assets managed within trust structures. If you’re selling property or investments through a trust, using a trusted tax calculator is crucial to estimate your new CGT liability.

The Practical Impact on Australian Families and Businesses

The reforms will reshape wealth, business, property, and succession planning in Australia.

– Families previously able to distribute large trust incomes among low- or no-income adult children—such as $200,000 split four ways—will now face a minimum $60,000 in tax (30%), eroding traditional advantages.

– Small business and asset protection: Owners using family trusts to shield business interests may need to rethink their structure. Flexibility remains, but tax benefits shrink.

– Property investors: Trust-held rental income or capital gains will attract higher taxes, making some real estate strategies less attractive when compared to direct ownership.

Staying ahead means evaluating whether asset structuring still delivers sufficient after-tax results and whether compliance costs are justified.

Key Dates and Implementation Timeline

- June 30, 2025: Annual deadline for every discretionary trust to prepare and lodge distribution resolutions.

- 2025-2026 tax year: Expected start of the 30% minimum tax on non-participating adult beneficiaries.

- Ongoing: ATO continues increased audit activity and compliance crackdowns, especially for distributions to lower-income adult children.

Preparation is key—reviewing structures well before deadlines can prevent rushed decisions and lasting tax consequences.

Expert Recommendations: Adapting to the New Reality

- Review trust structures with a qualified advisor to gauge reform impacts.

- Explore alternative business structures—companies, partnerships—or direct investment for better tax efficiency under new rules.

- Employ meticulous compliance: Draft, sign, and lodge all trust distribution resolutions by June 30, regardless of income.

- Weigh non-tax benefits: Asset protection, succession planning, and investment flexibility versus rising compliance and taxation costs. This is especially important for those managing business interests or property sales within a trust.

- Use an up-to-date tax calculator to forecast tax obligations and compare possible restructuring scenarios.

Frequently Asked Questions

What is the new 30% minimum tax rate for trusts?

Answer: As of 2025, trust distributions to non-participating adult beneficiaries must be taxed at a minimum rate of 30%, regardless of the recipient’s personal tax return bracket. This closes a traditional avenue for minimizing tax using trusts.

What happens if I miss the June 30 distribution resolution deadline?

Answer: Missed or improper resolutions mean all trust income is taxed at the top marginal rate (currently 47%), regardless of eventual distribution. The ATO is vigorously enforcing this rule.

How do these changes affect capital gains tax from properties held in a trust?

Answer: Expect less flexibility and potential for higher capital gains tax on assets sold through family trusts. The new regime targets perceived loopholes and taxes more trust-generated capital gains at higher rates.

Should I still use a trust for business or property?

Answer: Trusts may maintain advantages for asset protection, controlled succession, and business flexibility. However, with tax minimization benefits shrinking, consider reviewing your structure with a professional and using a reliable tax calculator to compare after-tax outcomes.

Where can I get help understanding my new obligations?

Answer: Consult a specialist tax advisor. You can also reference current ATO resources, review guides to trust compliance, and use digital tools or a modern tax calculator for immediate estimates and planning.